Lecture 21: Testing for Correlation#

STATS 60 / STATS 160 / PSYCH 10

Announcement:

Next week, guest lectures by Aditya and Prof Sun.

Randomized control trials!

Concepts and Learning Goals:

Hypothesis test for correlations

testing via simulation

permutation test

Estimating variability of correlation

simulation: “The bootstrap”

Bootstrap confidence intervals

Trends in multiple variables#

Until now we have been hypothesis testing for trends in a single variable:

AI vs. not photo challenge: proportion of correct guesses (the variable is \(x_i = 0/1\), depending on whether guess is right)

Discrimination against North Americans: proportion of North Americans (the variable is \(x_i = 0/1\), depending on whether the employee is North American)

Gettysburg address: length of word sampled (the variable is \(x_i = \text{word length}\))

Many times, we measure multiple variables, and we want to test for a trend in how they are associated.

“Can variable \(x\) actually help you predict variable \(y\)?”

Correlation#

Suppose that I have sampled \(n\) individuals from my population, and for each I have measured the values \((x_i,y_i)\).

For example:

Penguins: \(x =\) body mass, \(y=\) beak length

Medicine: \(x=\) blood pressure, \(y=\) age

Economics: \(x=\) years of education, \(y=\) salary

College admissions: \(x=\) SAT score, \(y=\) sophomore-year GPA

The correlation coefficient of \(x\) and \(y\) is the slope of the best-fit line for the standardized datasets \(x_1,\ldots,x_n\) and \(y_1,\ldots,y_n\).

where \(\bar{x},\sigma_x\) are the mean and standard deviation of the \(x\)’s, and \(\bar{y},\sigma_y\) are the mean of and standard deviation of the \(y_i\)’s.

Variability in the correlation coefficient#

Usually, we want to know the population value of the correlation coefficient: the ground truth value \(R\) across the whole population.

The correlation coefficient of our sample, \(\hat R_{n}\), is a function of our sample data, so it is random, and exhibits variability.

If we got a different sample, we could get a different value of the correlation coefficient.

Suppose that we compute the correlation coefficient for our sample, and see that it has value \(\hat R_n\).

If \(\hat R_n \neq 0\), is this a sign of an actual association, or is it just a coincidence?

How much variability is there in \(\hat{R}_n\)?

Testing for correlation#

Suppose that we compute the correlation coefficient for our sample, and see that it has value \(\hat R_n \neq 0\).

Is this just a coincidence? Or is the correlation a real pattern?

Let’s formulate this as a hypothesis testing problem:

Null Hypothesis: there is no correlation.

How can we compute the \(p\)-value?

We’ll use simulation!

FYI: if you are willing to make assumptions about the distributions of \(x,y\) under null, you can use a Chi-squared (\(\chi^2\)) test (outside the scope of this STATS60).

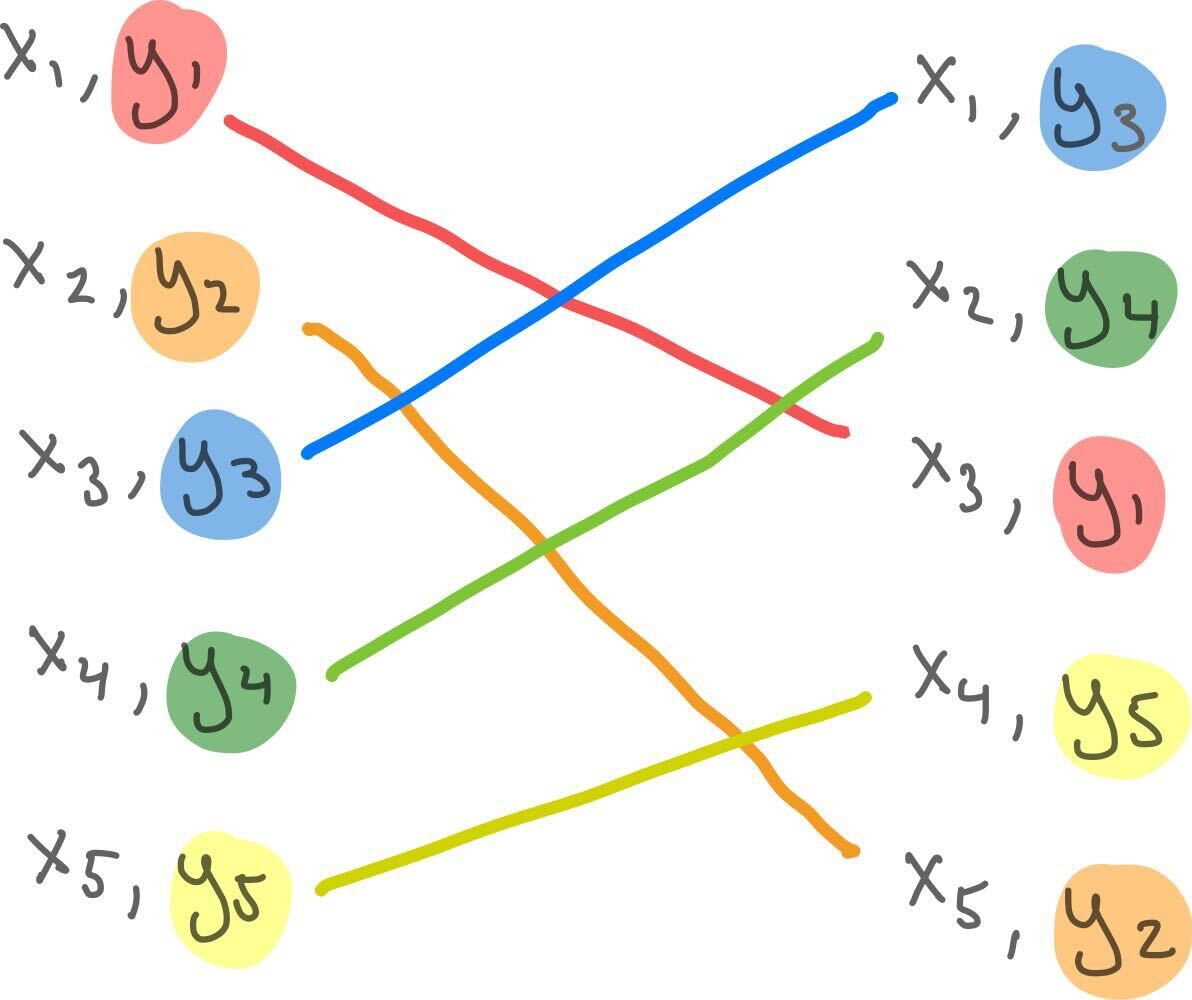

Permuting the datapoints#

Let’s assume, from now on, that our \(x_i\) and \(y_i\) are standardized.

Suppose there really is a positive association between \((x_i,y_i)\).

Now, what if we randomly shuffle or permute the \(y_i\), so that they are matched to a random \(x_j\)?

There’s almost certainly no correlation now!

Null hypothesis based on shuffling#

Suppose we have computed \(\hat R\) from our data. We want to know if \(\hat R\) reflects an actual trend, or if it is just noise.

Null hypothesis: the pairs \((x_i,y_i)\) are paired up totally randomly.

Question: Why is this null hypothesis saying that there is no real correlation?

Question: In plain English, what is the \(p\)-value of \(\hat{R}\)?

The null is saying there is no real correlation because if the pairing of \(x_i\) and \(y_i\) is arbitrary/random, there would almost certainly not be a linear relationship.

The \(p\)-value is the chance that you’d get this value of \(\hat{R}\), or a more extreme one, if the data were paired up by randomly shuffling.

Permutation test for correlation#

Suppose we have computed \(\hat R\) from our data. We want to know if \(\hat R\) reflects an actual trend, or if it is just noise.

Null hypothesis: the pairs \((x_i,y_i)\) are paired up totally randomly.

\(p\)-value: the chance that you’d get this value of \(\hat{R}\), or a more extreme one, if the data were paired up by randomly shuffling.

We’ll compute the \(p\)-value using a Permutation test, a test based on simulation:

Do some large number \(T\) of repetitions of the following experiment:

a. Randomly permute/shuffle the \(y_i\) so that each is paired with some random \(x_j\)

b. Compute and record the correlation coefficient for the shuffled dataset

Make a histogram of the correlation coefficient values for all \(T\) trials.

Decide the \(p\)-value for \(\hat R\) based on how extreme it is relative to the histogram:

If \(\hat R\) is positive, the \(p\)-value for \(\hat R\) is the fraction of histogram values larger than \(\hat R\) (or \(1/T\), if none are larger).

If \(\hat R\) is negative, the \(p\)-value for \(\hat R\) is the fraction of histogram values smaller than \(\hat R\) (or \(1/T\), if none are smaller).

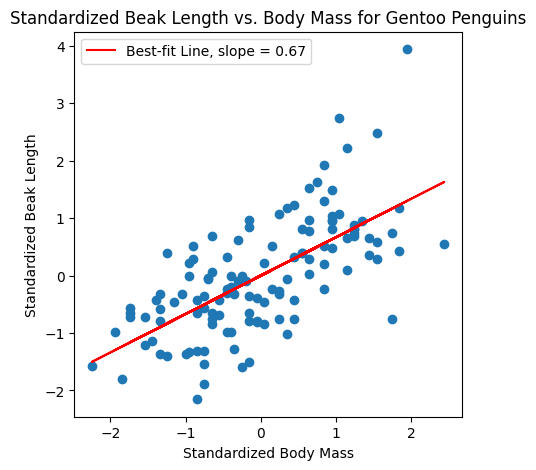

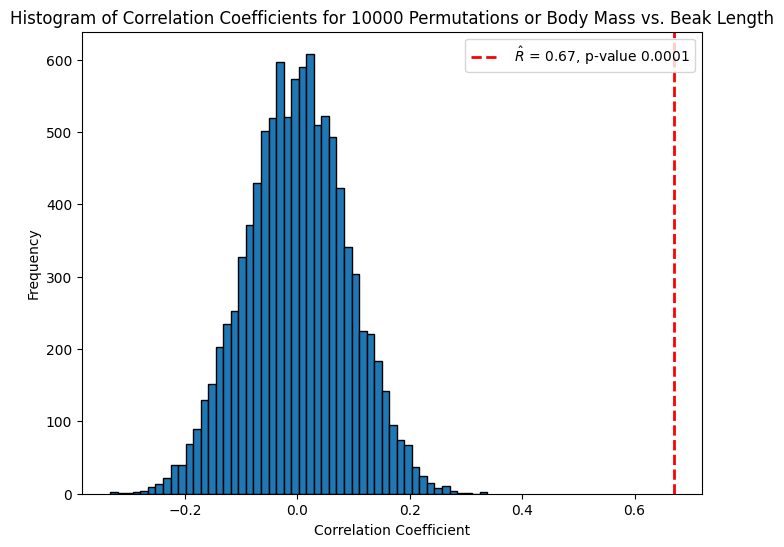

The penguins#

In Lecture 15, we computed a correlation coefficient of \(\hat R = 0.67\) for Gentoo Penguin body mass vs. beak length.

What is the \(p\)-value?

I ran a simulation with \(T = 10,000\) random permutations of the \(y_i\), and computed the correlation coefficient each time.

Below is a histogram of the \(T\) correlation coefficients for the random permutations.

Using the permutation test, the \(p\)-value is at most \(.0001\):

We conclude that \(\hat R\) is statistically significant at level \(\alpha = 0.05\) (or smaller).

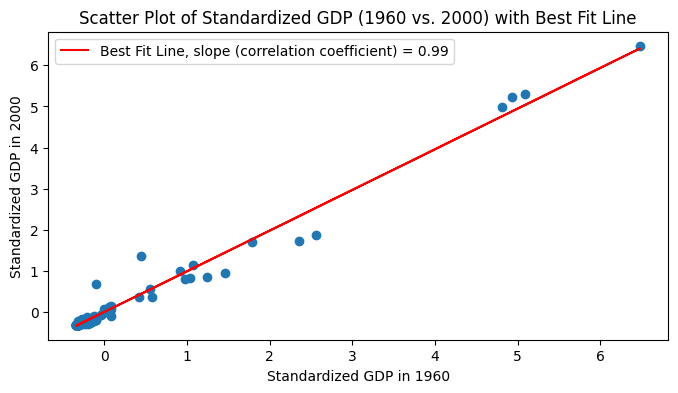

GDP in 1960 vs. 2000#

In Lecture 15 we also computed the correlation coefficient for the GDP of countries in 1960 vs. 2000.

We can do a permutation test to check if this value of \(\hat R\) is statistically significant.

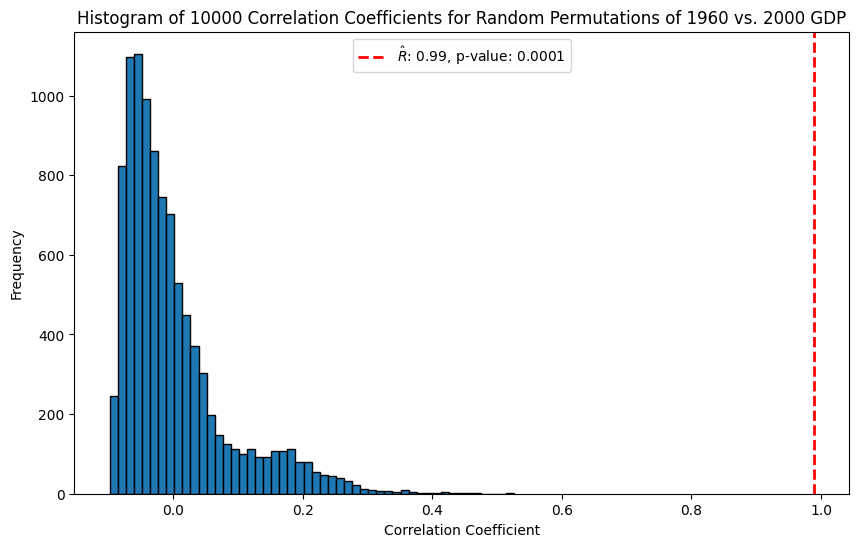

P-value for GDP correlation#

For \(T = 10,000\) permutations, the \(p\)-value is for the correlation coefficient of 1960 vs. 2000 GDP is \(1/10,000\):

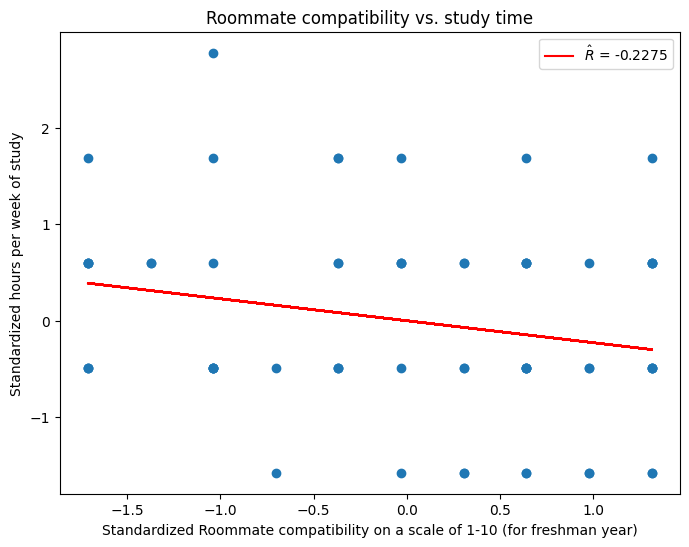

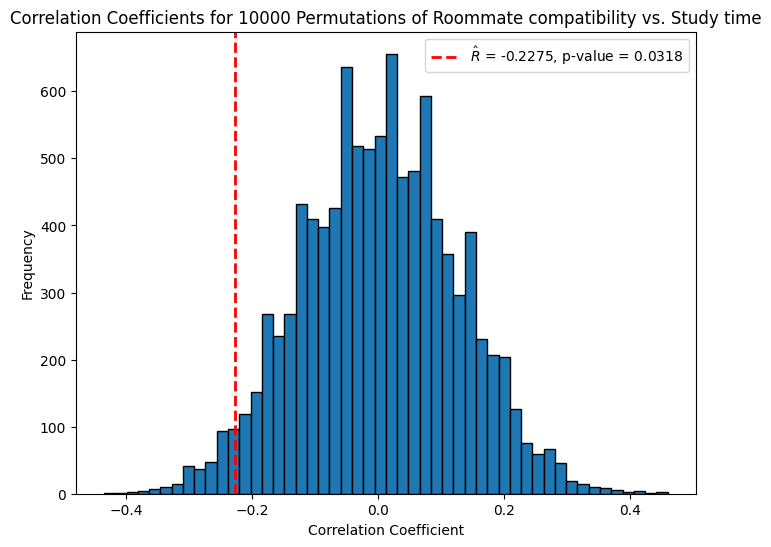

Are nerds lonelier?#

If we look at data from the course survey, we see a somewhat negative correlation between time spent studying and roommate compatibility. \(\hat R \approx -.2\)

\(p\)-value for lonely nerds?#

Via simulation, for a \(T = 10,000\)-trial permutation test, we verify that the \(p\)-value is \(\approx 0.03\), small enough that the trend is statistically significant at level \(\alpha = 0.05\):

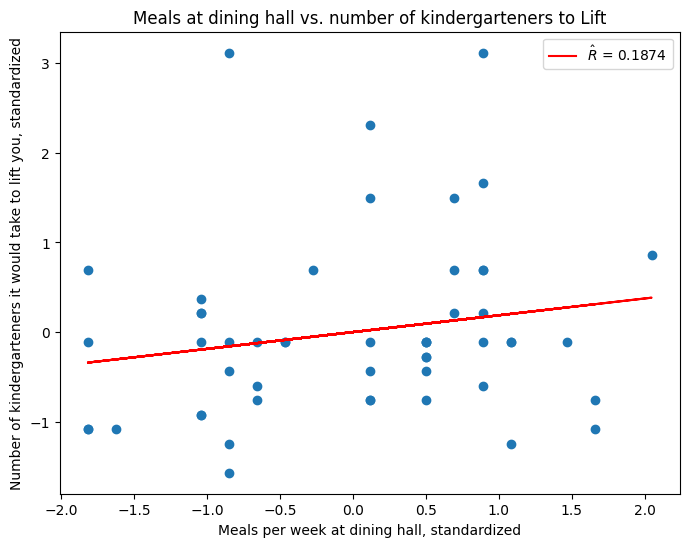

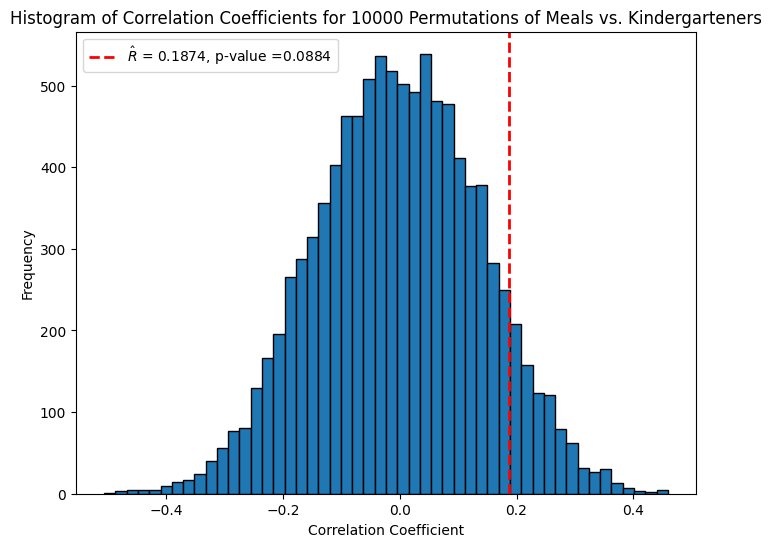

Are frequent diners too heavy for kindergarteners?#

We also see a positive correlation between the number of meals eaten at the dining hall each week and the number of (self-reported) kindergarteners it would take to lift you, \(\hat R \approx 0.2\).

\(p\)-value for meals and kindergarteners#

Via simulation, we see that this \(\hat R\) is not statistically significant at level \(\alpha = 0.05\), \(p\)-value \(\approx 0.08\).

Variability#

We computed \(\hat R_n\). But what about its variability?

Is \(\hat R_n\) being influenced by outliers?

If I had a slightly different sample, would my value of \(\hat R_n\) be dramatically different?

The permutation-test \(p\)-values only give us a sense of statistical significance of a correlation:

we can see how extreme \(\hat R_n\) is relative to a random shuffling of the data (no correlation)

we cannot see how \(\hat R_n\) would vary if we had a different sample from data with the same type of associative relationship.

How much variability in lonely nerds?#

The lonely nerd trend from the course survey was statistically significant.

However, what is the variability like?

Would the value of \(\hat R\) changed to a (smaller or larger) negative value if we had sampled differently?

How much smaller or larger?

Estimating variability with simulation#

We can use simulation to estimate variability too.

The best case scenario would be, if we have access to new samples from our population, just collect more samples and compute a fresh correlation coefficient a bunch of times.

But what if we don’t have access to new samples?

The following approach is called the bootstrap:

Start with our dataset \((x_1,y_1),\ldots,(x_n,y_n)\).

For some large number of trials \(T\):

a. Sample \(n\) pairs independently with replacement from the dataset: $\((x_{i_1},y_{i_1}),\ldots,(x_{i_n},y_{i_n})\)$

b. Compute and record the correlation coefficient of these pairs.

Form a histogram of the correlation coefficients from all \(T\) trials.

To get a \(1-\alpha\) confidence-interval around \(\hat R_n\), choose the interval around \(\hat R_n\) which contains \(1-\alpha\) fraction of the results from the \(T\) trials.

The Bootstrap#

To get a sense of the variability of \(\hat R_n\):

Start with our dataset \((x_1,y_1),\ldots,(x_n,y_n)\).

For some large number of trials \(T\):

a. Sample \(n\) pairs independently with replacement from the dataset: $\((x_{i_1},y_{i_1}),\ldots,(x_{i_n},y_{i_n})\)$

b. Compute and record the correlation coefficient of these pairs.

Form a histogram of the correlation coefficients from all \(T\) trials.

Question: why could this simulation give us a good sense of variability? Will it account for outliers?

There’s a reasonable chance that we’ll avoid any specific outlier in a trial when we sample with replacement: $\(\Pr[\text{avoid i }] = (1-\frac{1}{n})^n \approx e^{-1} \approx \frac{1}{3} \text{ when }n\text{ large.}\)$

If we take a \(2/3 \approx 66\%\) or larger confidence interval, it will likely contain the correlation coefficients from trial runs which avoid that outlier.

Question: will this always give us a good idea of the variability of \(\hat R_n\)?

Not necessarily; our sample could just be really weird.

A large enough sample probably reflects the population well enough that it should work pretty well. You can prove that this works with high probability when \(n\) is sufficiently large enough.

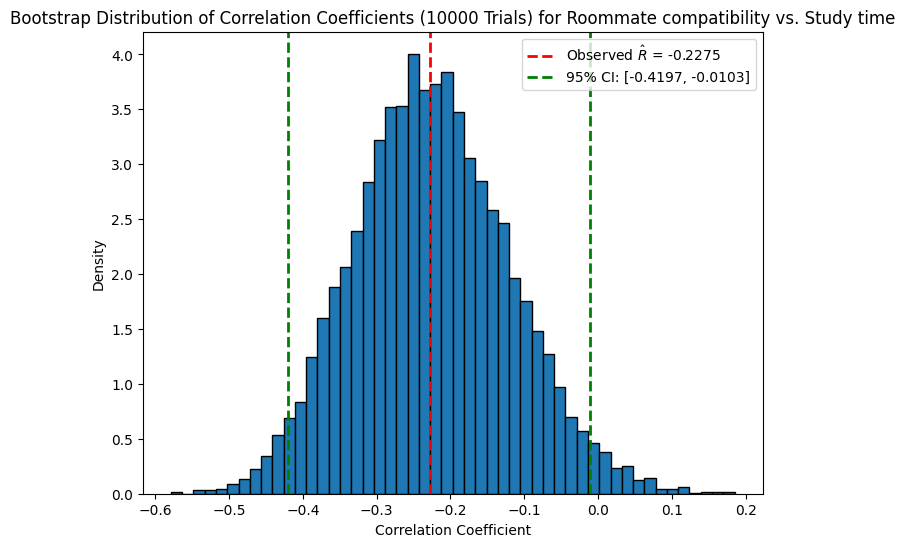

Simulation for variability in loneliness of nerds#

If we do a bootstrap simulation with \(T= 10,000\) trials, we can see that the confidence interval around \(\hat R\) is quite large, almost (but not quite) containing \(0\):

This gives us some sense of the variability of \(\hat R_n\).

Question: Are we sure this confidence interval is accurate for the population distribution of all Stanford students?

No. Our class (and the people who completed the course survey) might be a biased sample. But this does give a sense of variability within our class.

Correlation is not causation!#

Even though we can test for the statistical significance of a correlation, we do not know if this is a sign of causality.

If our \((x_i,y_i)\) pairs are observational, we don’t know if: a. \(x_i\) causes \(y_i\) b. \(y_i\) causes \(x_i\) c. both are caused by some unseen variable \(z_i\)

In medicine and other scientific research, this happens all the time:

For example, \(x_i =\) how much fiber you eat, \(y_i =\) cholesterol levels

We may observe a negative correlation between these variables a. Does a healthy diet cause low cholesterol? b. Are people who eat healthy also more likely to exercise, thereby controlling their cholesterol? (The unseen variable \(z_i =\) exercise)

Next week, experimental design and randomized control trials.

Recap#

Testing for correlation

Using simulation: permutation tests

Variability of correlation

Using simulation: “the bootstrap”